|

|

Does Monetary History Repeat Itself? - A Speech About Gold Manipulations by the Federal Reserve

Address of Wm. Mc C. Martin, Jr., Chairman, Board of Governors of the Federal Reserve System, New York City, June 1, 1965

OK: today, this sort of talk has been thrown out the window except in one area. People who think and write about gold do talk a great deal about this time and are very eager for historical information. This speech isn't as explosive as my discovery of the 1961 secret gold market manipulation memo I dug up a few weeks ago. But this speech clarifies the Federal Reserve's official thinking about how gold is to interact with this faux central bank's manipulation of interest rates and Treasuries. 1961 Top Secret Federal Reserve Gold Exchange Report

This is not wisdom of hindsight. Only a few weeks before the fateful decision was taken, the most eminent economist of the day stated that "for a country in the special circumstances of Great Britain the disadvantages (of devaluation) would greatly outweigh the advantages" and he concurred with his colleagues in rejecting the idea. Despite the ‘disadvantages' being so great, there was one major advantage to England debasing the pound, the thing used to determine all international trade values: Britain had to direct trade outwards, not inwards. Repeatedly, the US did the same thing. That is, we debased the currency at various intervals in a vain attempt at fixing our trade problems via monetarism.

I find it very interesting to go into the original speeches and documents of the Federal Reserve, this opens many windows in thought. Reading summaries don't do it like reading the originals! Interlacing these speeches across the decades and then tying it into today's news is how we weave history rather than simply glossing over it all. I found the above speech by the future head of the Reserve from back in the Great Depression. This guy saw all of this up close, he was very much involved in it from the beginning until the total collapse of the US gold system, years later. This is why he tries to give this speech, wrapping up all his previous experience. He is tormented by the idea, he is seeing ‘history' a second time for he worked on the process to bail out Britain in the Great Depression. This is why he talks about gold so much, after him, gold is barely mentioned or even derided or mocked. BUT HE TOOK ALL OF THIS VERY SERIOUSLY! His name was John Maynard Keynes. And soon afterwards, another great British economist, Lionel Robbins, declared that "no really impartial observer of world events can do other than regard the abandonment of the Gold Standard by Great Britain as a catastrophe of the first order of magnitude." This was long before the final consequences of that step had become apparent - the political weakening of the "West which followed its economic breakdown and which contributed to the success of the Nazi revolution in Germany, and thus eventually to the outbreak of the Second World War and to the emergence of Communism as an imminent threat to world order. As if neither Keynes, the founder of the anti-classical school of economics, nor Robbins, the leader of the neo-classical school, ever had spoken, some Keynesian and neo-classicist economists-fortunately with little support at home but with encouragement from a few foreign observers-are urging us to follow the British example of 1931 and to act once more in a way that would destroy a payments system based on the fixed gold value of the world' s leading currency. In doing so, they not only show that they have not learned from monetary history; they also impute to our generation even less wisdom than was shown in the interwar period. Wow! He is certainly battling on behalf of a secure, even-keeled, stable GOLD STANDARD, isn't he? His contemporaries felt the loss of the British support of the gold standard was a disaster. Note also, the reference to ‘Keynesian and neo-classicist economists-FORTUNATELY WITH LITTLE SUPPORT AT HOME but encouragement from a few foreign observers-ARE URGING US TO FOLLOW THE BRITISH EXAMPLE OF 1931…'-- Martins Jr is of the old school. Yet, knowing all of this, he slides down the same ramp leading to the destruction of the currency. Even as he was sweating his way through this summer speech, the destruction of the dollar was gathering steam. Thanks to the Vietnam War. See how he chides people demanding the US abandon gold entirely! He openly says, ‘They have NOT learned from monetary history!' and is furious that these upstarts are mocking him and his generation for being foolish when they were struggling to right a ship that was sinking. Martin Jr's main problem here is, he doesn't analyze the problem from the point of view of imperial overreach and rot. Britain was already being pushed downstairs by Germany, Japan and above all, the US itself. All were taking away British markets and were invading Britain's home markets before WWI broke out. I would suggest, one of the major causes of WWI was Germany surpassing England in industrial development and trade. The British Government in 1931, and the U. S. Administration in 1933, can rightly be accused of underestimating the adverse international effects of the devaluation of the pound and the dollar. But at least they had some plausible domestic grounds for their actions. They were confronted with a degree of unemployment that has hardly ever been experienced either before or after. They were confronted with disastrously falling prices, which made all fixed-interest obligations an intolerable burden on domestic and international commerce. They were confronted with a decline in international liquidity, which seemed to make recovery impossible. Neither Keynes nor Robbins have denied that, from a purely domestic point of view, there was some sense in devaluation. In the United States of 1933, one worker out of four was unemployed; industrial production was little more than half of normal; farm prices had fallen to less than half of their 1929 level; exports and imports stood at one-third of their 1929 value; capital issues had practically ceased. In such a situation, any remedy, however questionable, seemed better than inaction. They had the identical problem we have today: a steep decline in INTERNATIONAL LIQUIDITY. Of course, the US was the wellspring of liquidity and when countries borrowing money ceased to send payments back to the US, the entire structure of support of lending collapsed! You can't borrow and not repay and then expect more loans to infinity. Nor can anyone spent to infinity while never repaying. WWI was a horror. Due to the creation of the Federal Reserve, the warring states could borrow near-infinite money to fight. Instead of balancing real deficits with future desires, they simply poured money into the mess until all sides were nearly totally bankrupt. Then, to rebuild, all the same empires ran to the US to demand MORE loans so they could support each other's economies. And the debts were just too much. In the Britain of 1931, things were not quite as bleak as in the United States of 1933; but fundamentally, the economic problems were similar. Ever since 1925, the British economy had failed to grow, and by 1931, one out of five workers had become unemployed, exports-far more important for the British economy than for our own-had declined by nearly one-half, and most observers believed that over-valuation of the British pound was largely responsible for all these ills. Can anybody in good faith find any similarity between our position of today and our position of 1933, or even the British position of 1931 ? Now, who is exactly like Britain, today? Why, Japan! Back in 1931 and even in 1965, we made most of the industrial goods we consumed. We even consumed our own oil! So it was OK for us to help England, who needed to export much more than us, to do this. But who was England to export to? The US suddenly had to fend off this export giant! This is what the trade barriers of the 1930's were all about. Our own industrial base would have vanished by 1941 if we let the British weaken the pound while keeping the dollar strong! So we debased the dollar to the same degree [to the rage of the British, I dare say!]. In 1931 and 1933, an increase in the price of gold was recommended in order to raise commodity prices. Today, a gold price increase is recommended as a means to provide the monetary support for world price stability. In 1931 and 1933, an increase in the price of gold was recommended in order to combat deflation; today it is recommended in effect as a means to combat inflation. In 1931 and 1933, an increase in the price of gold was recommended as a desperate cure for national ills regardless of its disintegrating effect on world commerce; today it is recommended as a means to improve integration of international trade and finance. Can there be worse confusion? This is a most interesting paragraph! In the Great Depression, gold prices were unilaterally and suddenly jacked up in price, and of course, Martin Jr doesn't mention the confiscation of gold before this happened….YIKES…the devaluation of the paper representing gold values was not received with joy by either gold holders who lost their gold before the sudden devaluation of the paper money, nor by trade rivals who had carefully held gold dollar certificates issued all the way up until 1929 by the US Federal Reserve! These were supposed to ‘give gold on demand' but the holders assumed, the value of gold to paper would be stable, not cut by nearly half! This certainly was ‘theft'. And in England and the US, both central banks did this suddenly and viciously, there was no room for letting anyone prepare for this. Since it was theft, it had to be presented as a fait accompli. C Martin Jr's testimony to Congress in 1934:

The hope was to finesse the queer non-central, central bank. The crisis of the Great Depression saw the powers of the Fed grow, not wither. A queer thing happened to us: We see from these speeches both in 1934 and 1965, that the Fed is supposed to regulate many markets. Such as STOCK MARKET MARGINS. This was to prevent the wild growth of leveraged betting. This is precisely what has totally collapsed. Instead of restricting lending, the Fed enabled wild lending. This caused the many bubbles that are now burst and which have ruined our entire economic system. Instead of improving controls, the Fed threw away controls and did this in tandem with Congress and our Presidents throwing all caution to the winds as everyone tried to live off of credit, not savings. True, most advocates of an increase in the price of gold today would prefer action by some international agency or conference to unilateral action of individual countries. But no international agency or conference could prevent gold hoarders from getting windfall profits; could prevent those who hold a devalued currency from suffering corresponding losses; could prevent central banks from feeling defrauded if they had trusted in the repeated declarations of the President of the United States and of the spokesmen of U. S. monetary authorities and kept their reserves in dollars rather than in gold. To this day, the French, Belgian, and Netherlands central banks have not forgotten that the 1931 devaluation of sterling wiped out their capital; and much of the antagonism of those countries against the use of the dollar as an international reserve asset should be traced to the experience of 1931 rather than to anti-American feelings or mere adherence to outdated monetary theories. Please remember this paragraph, anyone who is ‘hoarding' gold must be aware, the government views you all as enemies of the State and will move to fix this if they see they need the gold! Notice how he talks about preventing gold speculators from profiting from higher values of gold vis a vis, currencies! Also, notice the comments about many European nations leery of using the US dollar as a trade value guide. Instead, they want gold to do this. We assume the transition from the British pound trade regime to the US $ regime was smooth. It wasn't, not at all. When this 1965 speech was being made, the value of gold was not as volatile as it was going to be very shortly. The Losing Battle to Fix Gold at $35 - John Paul Koning - Mises Institute

Ah, I see the sudden spike in 1960! The Gold Pool was launched in utmost secrecy at first, by 1961. The Pool was drained by Charles de Gaulle in 1968. We can see how slight differentials in gold values between the US and London could be exploited for small but secure sums. We also note that no gold actually changed hands in these ‘deals'. This was done purely via paper shuffling. This is the infant ‘Derivatives' market and is the philosophical creation point of the entire super-structure of not only derivatives but also, hedging businesses. The fact that gold market instabilities as the world vacillated between the British and the US trade valuation systems, was the creation of the entire business of derivatives is most interesting! For the Derivatives Beast, once it ceased to play this small game in a fairly stable system, has created immense instability as everything rocks back and forth with increasing violence, between all sorts of unstable values and systems! But most importantly, no international agency or conference could prevent a sudden large increase in the gold price from having inflationary consequences for those countries that hoarded gold, and deflationary consequences for those that did not. And the gold holding countries are precisely those whose economies are least in need of an inflationary stimulus since they are most prosperous-not prosperous because they are holding gold, but holding gold because they are prosperous; in contrast, those that do not hold gold are most in need of further expansion. Hence the inflationary and deflationary effects of an increase in the price of gold would be most inequitably and most uneconomically distributed among nations. If we were to accept another sort of advice given by some experts, we might repeat not the mistakes of 1931-33 but those of earlier years. We are told that a repetition of the disaster of the Great Depression could be averted only, or at least best, by returning to the principles of the so-called classical gold standard. Not only should all settlements in international transactions between central banks be made in gold; but also the domestic monetary policy of central banks should be oriented exclusively to the payments balance, which means to changes in gold reserves. Whenever gold flows out, monetary policy should be tightened; whenever it flows in, it should be eased. This is not the place to discuss whether this pure form of gold standard theory has ever been translated into practice. I doubt that any central bank has ever completely neglected domestic considerations in its monetary policy. And conversely, we do not need to adhere to an idealized version of the gold standard in order to agree that considerations of international payments balance need to play a large role in monetary policy decisions. But even strict adherence to gold standard principles would not guarantee international payments equilibrium. As a great American economist, John H. Williams, put it in 1937:

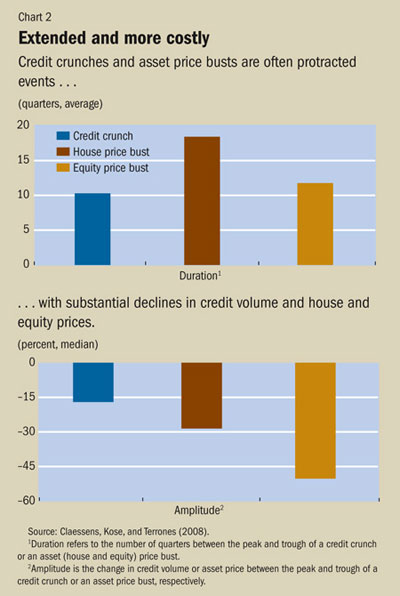

Gold cannot prevent bubbles or crashes. NOTHING can do this from the outside. The ONLY thing that prevents this is for regulators to really regulate a very simple thing: the level of savings, if it is collapsing while lending is progressing at higher and higher levels, the only way to stop this is to force interest rates upwards AND increase the reserve ratio required by the banks. For example, China did this aggressively last year! From the IMF: Finance & Development, December 2008 - When Crises Collide

Even countries that advocate a return to gold standard practices do not practice what they preach. Gold reserves of some Continental European countries have been rising strongly and continuously for many years, and according to the rules, these countries should follow a clearly expansionary policy. But in order to offset inflationary pressures, they have done exactly the opposite-and who is there to blame a country that wishes to assure domestic financial stability even at the expense of endangering equilibrium in international payments? But obviously, if we permit one country to violate the rules of the gold standard in order to avert domestic inflation, we must also permit another country to violate those rules in order to avert domestic deflation and unemployment. In other words, we must agree that a country may be justified in avoiding or at least modifying a tightening of monetary policy even though its gold reserves are declining, if otherwise it were to risk precipitating or magnifying a business recession. True, this deviation from gold-standard rules could be carried too far. Domestic developments might be taken as a pretext to avoid an unpopular monetary move, although the payments situation would seem to demand it and although the action would be unlikely to be damaging to the domestic economy. But the possibility of abuse and error is inherent in all human decision, and just as no sane observer would ascribe infallibility to the decisions of central bankers, neither should he ascribe infallibility to a set of rules. HAHAHA! Some countries might deviate from the gold standard rules….so they can fight futile wars against the Vietnamese peasants! Wow! The US hoarded gold during the Great Depression. The central bank here did this via confiscation of gold via devaluing the currency after laws were passed, outlawing gold trade/redeeming by US citizens EVEN WHILE ALLOWING FOREIGN GOVERNMENTS THE RIGHT TO DO THIS! This was a very significant loss of citizen sovereignty. Few experts today would want to argue that it was right for the German Reichsbank in 1931, in the middle of the greatest depression that ever hit Germany, to follow the gold standard rules by raising its discount rate to 7% merely in order to stem an outflow of gold; or that it was right for our own Federal Reserve to take similar restrictive action, for the same reason, in the fall of 1931. Except Germany was punished and the US was rewarded. Germany lost WWII and we won and we imposed Bretton Woods on the rest of the world. And just as the success of monetary policy cannot be guaranteed by an abdication of discretion in favor of preconceived gold-standard rules, it cannot be guaranteed by following the advice of those who would shift the focus of policy from national agencies to an international institution. Surely, international cooperation should be encouraged and improved whenever possible. And the functions of the International Monetary Fund might well be enlarged so as to reinforce its ability to act as an international lender of last resort and as an arbiter of international good behavior. But no institutional change can exclude the possibility of conflicts between national and international interests in specific circumstances. Moreover, there is no reason to believe that such conflicts would necessarily be resolved more wisely, more speedily, and with less rancor and dissent if they were fought out in the governing body of some supra-national bank of issue rather than by discussion and negotiation among national authorities. It is true that such discussion and negotiation may prove fruitless and that inconsistent decisions may be taken on the national level. But similarly, lack of consensus within a supranational agency may result in a paralysis of its functions, and the effects of such paralysis could well be worse than those of inconsistent national actions. If then we doubt the wisdom of the three most fashionable recent proposals-to increase the dollar price of gold, to return to pure gold-standard principles, or to delegate monetary policy to an international agency-what should be our position? And what is the outlook for solving present and future difficulties in international monetary relations, and thus for avoiding a repetition of the disasters of 1929-33? And here enters the New World Order: the Bilderberg secret meetings, the war mongers put in charge of the IMF and World Bank, the Security Council overriding all UN debates and choices, the World Trade Organization meetings, the various incarnations of the G7 meeting systems, etc. These proliferated after WWII. Their goal is pretty obvious: to use the US as the military arm of global domination by the upper class elites of the Empires of Europe and the US. With the entire system hinged on the floating currency values of the US $, this means the US gets to remain a pivot for world trade and world power no matter what. And the ruling elites can ignore debt levels, spending limits, etc, etc, while spending wildly on US arms and US imperial proposals across the planet! The hubris in all this is obvious: it is destroying the United States as an economic power. This is why Hillary had to hike right off the bat to China and Japan to give them whatever they demanded so they will allow this stupid system to continue. In my judgment, it is less fruitful to look for institutional changes or for a semi-automatic mechanism that would guarantee perennial prosperity than to draw from interwar experience some simple lessons that could save us from repeating our worst mistakes. First, most observers agree that to a large extent the disaster of 1929-33 was a consequence of maladjustments born of the boom of the twenties. Hence, we must continuously be on the alert to prevent a recurrence of maladjustments-even at the risk of being falsely accused of failing to realize the benefits of unbounded expansion. Actually, those of us who warn against speculative and inflationary dangers should return the charge: our common goals of maximum production, employment, and purchasing power can be realized only if we are willing and able to prevent orderly expansion from turning into disorderly boom. Barely had he said all this, the gold situation went off the cliff and gold began to pour out of Fort Knox, people in America figured out how to use Swiss bank accounts to buy gold in Europe! This led to the government demanding this stop. Escape from the US anti-gold prison was made as difficult as possible. But the ruling elites, themselves, were the main ones doing this! HAHAHA. Anyone who globe-trotted had to do this! Second, most observers agree that the severity of the Great Depression was largely due to the absence of prompt antirecession measures. In part, the necessary tools for this were not then available nor were their potentialities fully understood. Today it is easy to understand where observers went wrong 35 years ago. But it is less easy to avoid a repetition of the same mistake; we always prefer to believe what we want to be true rather than what we should know to be true. Here again, we need most of all eternal vigilance. But we must also be ready to admit errors in past judgments and forecasts, and have the courage to express dissenting even though unpopular views, and to advocate necessary remedies. Unlike Bernanke, at least he is humble about all this! He also knows that restarting lending via overcoming the process of deflation is a tricky thing and perhaps, hard to avoid.

Third, and most importantly, most observers agree that the severity of the Great Depression was due largely to the lack of understanding of the international implications of national events and policies. Even today, we are more apt to judge and condemn the worldwide implications of nationalistic actions taken by others than to apply the same criteria to our own decisions. Recognition of the close ties among the individual economies of the free world leads to recognition of the need to maintain freedom of international commerce, This means not only that we must avoid the direct controls of trade and exchange that were characteristic of the time of the Great Depression. It means also that we must avoid any impairment of the value and status of the dollar, which today acts-just as sterling did until its devaluation in 1931-as a universal means of international payment between central banks as well as among individual merchants, bankers, and investors. If the dollar is to continue to play its role in international commerce, world confidence in its stability must be fully maintained; the world must be convinced that we are resolved to eliminate the long-persistent deficit in our balance of international payments. The measures taken in accordance with the President's program of February 10, 1965, have so far been highly successful. But some of these measures are of a temporary character, and these include the efforts of the financial community to restrain voluntarily the expansion of credit to foreigners. We should not permit the initial success of these efforts to blind us against the need of permanent cure. When the need to have a stable dollar and to keep gold stable in price collapsed even as Mc C Martin Jr was talking that day, so long ago. As more soldiers poured into Indochina, to slog through the jungles there, all hope of stabilizing the dollar rotted in the verdant overgrowth in SE Asia. Some observers believe that our responsibility for maintaining the international function of the dollar puts an intolerably heavy burden on our monetary policy; that this responsibility prevents us from taking monetary measures which might be considered appropriate for solving domestic problems. I happen to disagree with that view. I believe that the interests of our national economy are in harmony with those of the international community. A stable dollar is indeed the keystone of international trade and finance; but it is also, in my judgment, the keystone of economic growth and prosperity at home. Yet even if I were wrong in this judgment, and if indeed an occasion arose when we could preserve the international role of the dollar only at the expense of modifying our favored domestic policies-even then we would need to pay attention to the international repercussions of our actions. We must consider these international effects not because of devotion to the ideal of human brotherhood, not because we value the well-being of our neighbors more than our own. How sad, this all is! American WWII idealism crashing into the reality of the Vietnam war! We were not devoted to any sort of ideal of human brotherhood…we were devoted to murdering massive numbers of civilians because they resisted our colonial rule! U.S. debt is losing its appeal in China - International Herald Tribune

It is quite comical that the US is now begging communist China for loans! The US is paying paper to China. China has not asked for gold. The US pretends the gold we still hold in Fort Knox is non-real and has no bearing on our debts we owe China. But when the value of gold in the open market reaches the point where that gold is worth the same as China's dollars, namely, nearly $2 trillion, the Chinese will have the right to demand we pay up in gold. This will begin the New World Order of the Old Gold Reserve System. Of course, the US will refuse to do this and will challenge China to war. This is why pretending gold is meaningless is stupid. We must face reality here. If all currencies become a collective joke as they all try to race to the bottom and all banks offer 0% on savings, we will have a total collapse of savings across the entire planet and if we think the banking system is dead, wait three years! It will be ‘deader'. We must do so because any harm that would come to international commerce and hence to the rest of the world as a result of the displacement of the dollar would fall back on our own heads. In the present stage of economic development we could not preserve our own prosperity if the rest of the world were caught in the web of depression. Recognition of this inter-dependence gave rise to the Marshall Plan-in my judgment the greatest achievement of our postwar economic policy. It should not have taken the Great Depression to bring these simple truths home to us. Today, as we approach the goal of the "Great Society-to make each of our citizens a self-reliant and productive member of a healthy and progressive economic system-we can disregard these truths even less than we could a generation ago. By heeding them instead, we will have a good chance to avoid another such disaster. If monetary history were to repeat itself, it would be nobody's fault but our own. The utter rotting away of the US imperial financial and industrial base began long, long ago. The story of how gold went from being the basis of our financial systems to being mocked and marginalized is only one aspect of how our system went from functional to ruins. Basically, we wanted something for nothing. We wanted to rule the world and not pay the price. We thought, if we got rid of the inconveniences of the gold system, we could balance things while spending money recklessly. This was very childish. And the commentary, at the top of our political system, reflects this. It is very childish. Periodically, someone tries to break through all this and sound the alarm. Obviously, Ron Paul and Kucinich try this in vain. Cartoonists notice that we can't fix too much debt by adding even more debts. But not the ruling elites. They cling to this absurd notion no matter what. The Long Wave Analyst: Economic Forecaster and Interpreter of the Kondatieff Cycle

And the above is yet another attempt at telling our present rulers the truth. Not that anyone listens anymore. When Consumers Cut Back - A Lesson From Japan - NYTimes.com

If there really are no savings holding up the banking system, then what does? And the answer is obvious: GOLD. It sits there in a number of vaults, waiting in the dark. It will soon step back onto the world stage to after the Fat Lady sings. |

|

|

Here is part II of the Mc C. Martin Jr speech given in 1965, right when the Great Society and the Vietnam War began to destroy the finances of our government and debase the value of the currency. The first half of the speech is about history and fears of the Great Depression. The second half of the speech digs into the matter of gold markets, European powers and France's need to boost gold reserves. Also, he talks about Keynes and the new system which basically says, create inflation deliberately and depressions will magically vanish. We must read this entire speech for it opens the door to the way the present financial professors and movers and shakers operate today, how they were trained and think.

Here is part II of the Mc C. Martin Jr speech given in 1965, right when the Great Society and the Vietnam War began to destroy the finances of our government and debase the value of the currency. The first half of the speech is about history and fears of the Great Depression. The second half of the speech digs into the matter of gold markets, European powers and France's need to boost gold reserves. Also, he talks about Keynes and the new system which basically says, create inflation deliberately and depressions will magically vanish. We must read this entire speech for it opens the door to the way the present financial professors and movers and shakers operate today, how they were trained and think.

The IMF wishes to talk about history, too! HAHAHA. It is rather amusing, seeing how this is being done from scratch, basically. They want to figure out the pattern of bubble/collapse. Lots of people play this game. There certainly is a cycle and it seems to be ‘generational' in nature but there is something deeper at work. I referred to the extremely ancient 14 year cycle of ancient Egypt. They thought this cycle to be so important, they made it a part of their religion.

The IMF wishes to talk about history, too! HAHAHA. It is rather amusing, seeing how this is being done from scratch, basically. They want to figure out the pattern of bubble/collapse. Lots of people play this game. There certainly is a cycle and it seems to be ‘generational' in nature but there is something deeper at work. I referred to the extremely ancient 14 year cycle of ancient Egypt. They thought this cycle to be so important, they made it a part of their religion. Look at those graphs! I have contended for years that Japanese savings have collapsed due to the ZIRP system imposed on them. Wages fall, buying falls but also, savings collapse! In the US, it is already at zero. Soon, it will be there in Japan, too. The US has not rewarded savers in a long time. We were forced to hand money over to the stock markets and hope the stocks rise based on leverage bids! This, in turn, caused the financial meltdown when Japan ceased to be able to fund loans to hedge funds playing Wall Street games across the planet.

Look at those graphs! I have contended for years that Japanese savings have collapsed due to the ZIRP system imposed on them. Wages fall, buying falls but also, savings collapse! In the US, it is already at zero. Soon, it will be there in Japan, too. The US has not rewarded savers in a long time. We were forced to hand money over to the stock markets and hope the stocks rise based on leverage bids! This, in turn, caused the financial meltdown when Japan ceased to be able to fund loans to hedge funds playing Wall Street games across the planet.