Send this article to a friend:

January

08

2024

|

Send this article to a friend: January |

|

Pressing for Yet More

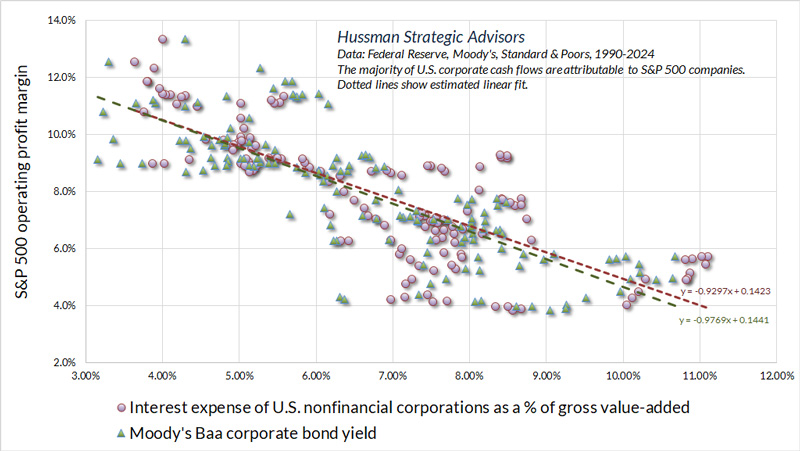

On December 6, the S&P 500 set the most extreme level of valuations on record, exceeding both the 1929 and 2000 market peaks on measures that we find best-correlated with actual, subsequent 10-12 year S&P 500 total returns across a century of market cycles. Reliable valuation measures are enormously informative about both long-term investment returns and the potential depth of market losses over the completion of any given market cycle. At the same time, valuations are of strikingly little use in projecting market outcomes over shorter segments of the market cycle. Investor psychology – the desire to speculate, or the aversion to risk – has a much stronger impact, which is why we also have to attend to factors including market internals, sentiment, short-term overextension / compression, and monetary policy (while unfavorable market internals dominate monetary easing, favorable internals amplify it). Amid the untethered enthusiasm about artificial intelligence, and prospects for deregulation and lower corporate taxes, it’s worth repeating that despite all the society-changing innovations of the past 20-30 years, both GDP and S&P 500 Index revenues (which include the impact of stock buybacks) have grown at an average rate of only about 4.5% annually. That’s slower, not faster, than the growth rate during the preceding half-century. Yes, the largest companies are very profitable, but that’s nearly always true at speculative extremes. That cohort of mega-cap companies is constantly changing, and except on their approach to extremes like 1929, 1972, 2000, and today, the companies with the largest market capitalizations have historically gone on to lag the S&P 500 over time. Investors regularly forget that the central feature of free-enterprise is the continual emergence of innovation-driven “new eras” in which both profit margins and growth rates are trajectories rather than durable numbers. As I reviewed in last month’s comment, Ring Out Wild Bells, the primary driver of rising profit margins since 1990 has not been rapid productivity growth or higher EBIT margins (earnings before interest and taxes). The simple reality is that most of the expansion in profit margins since 1990 is explained by falling interest expense, thanks to persistently declining interest rates that companies temporarily locked in at the 2020-2021 lows.

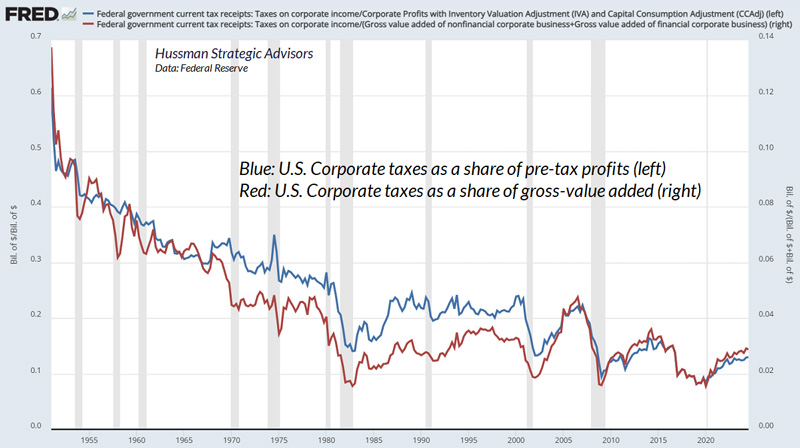

Meanwhile, most of the historical impact of corporate tax reductions was reflected in profit margins by the early 1980’s. Even if corporate taxes were reduced by one-third from here, and assuming those tax cuts were sustained permanently, the value of that tax reduction would amount to just 4% of market capitalization, and after-tax profit margins would increase by less than 1%.

Having priced the stock market at elevated multiples of record earnings, investors now require profit margins to sustain record highs permanently – simply for growth in earnings and payouts to match the 4.5% revenue growth rate of recent decades, and they require the S&P 500 price/revenue ratio to remain at a permanently high plateau, three times its historical norm. Given our own 4-year baseline expectation for real GDP growth of just 1.5% (see The Turtle and the Pendulum), even 4.5% nominal growth would require either a 3% inflation rate in the coming years, or a 2% inflation rate coupled with a jump in productivity that fully restores the 1948-2000 average. One might hope for higher inflation, imagining that it might produce higher nominal growth and accompanying market returns, but that would require valuations to remain at record extremes. Unfortunately, valuations are the first casualty of persistent inflation. In fact, except when valuations have been at least 25% below historical norms, the S&P 500 has lagged Treasury bills, on average, when consumer price inflation has been anything over 4%. There’s no question that investors are eager to justify record valuation multiples by appealing to the growing share of technology companies in the S&P 500. Yet the technology sector itself is trading at the highest multiple to revenues on record. Meanwhile, the growth rate of overall S&P 500 revenues, which include the technology sector, is belowhistorical norms while the S&P 500 price/revenue multiple is three times its historical norm, easily eclipsing the 1929 and 2000 peaks. Still, for the moment, neither valuations nor arithmetic matter to investors. As Galbraith observed, “As long as they are in, they have a strong pecuniary commitment to belief in the unique personal intelligence that tells them that there will be yet more.” Hence the sort of magazine cover Barron’s ran only a week after the S&P 500 set its recent record high – “Embrace the bubble.”

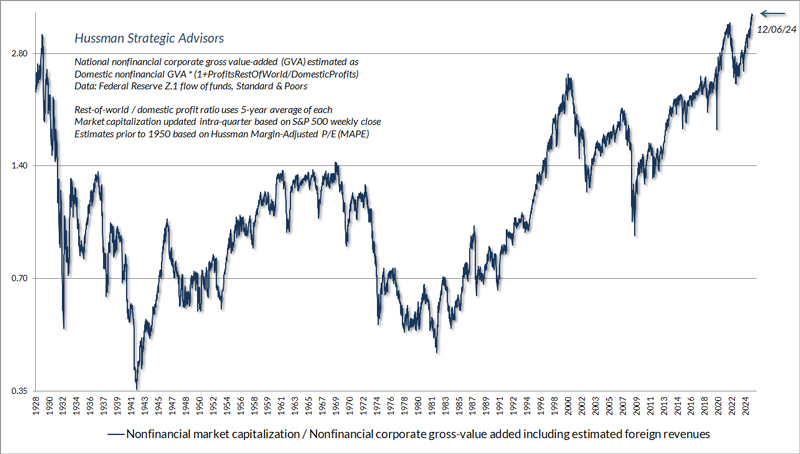

A review and update of market conditions Our most reliable gauges of market valuation continue to trace out what I view as the extended peak of the third great speculative bubble in U.S. history – implying the most negative prospects for expected S&P 500 total returns on record. Still, valuations are not a timing tool. Given the continued unfavorable (and deteriorating) status of our key gauge of market internals, along with a continued preponderance of overextended warning syndromes, our investment outlook remains clearly negative. Although there are many points in history when the S&P 500 advanced despite a combination of elevated valuations and unfavorable internals, including the approaches to the 1972, 2000 and 2007 market peaks, there’s no question that an additional speculative tailwind was added in 2024 by Wall Street’s exuberance about AI and its eagerness for profit-centric policy shifts. As I noted in the September Asking a Better Question, given the internal divergences we observe (which have worsened considerably in recent weeks), my impression is that our gauge of internals remains unfavorable precisely because of the internal divergences it is designed to measure. It’s the wrong question to ask how we might cleverly dart between a defensive outlook and a bullish one amid historically ominous market conditions. The better question was how to vary the intensity of a valid defensive outlook, in a way that can be expected to benefit even in a further advance, provided only that the market fluctuates along the way. At present, based on the hedging adaptation we implemented in late-September, we aren’t inclined to tighten our put option hedges further the event of a continued market advance. Our outlook is clearly bearish here, but it’s not one I expect to amplify at the moment. As I detailed in Subsets and Sensibility, one of the features of this hedging adaptation is that it reduces our risk of “fighting” market advances even in market conditions that are quite hostile from a historical perspective. With respect to prevailing conditions, the chart below reviews our most reliable gauge of market valuations in data since 1928: the ratio of nonfinancial market capitalization to gross value-added (MarketCap/GVA). Gross value-added is the sum of corporate revenues generated incrementally at each stage of production, so MarketCap/GVA might be reasonably be viewed as an economy-wide, apples-to-apples price/revenue multiple for U.S. nonfinancial corporations.

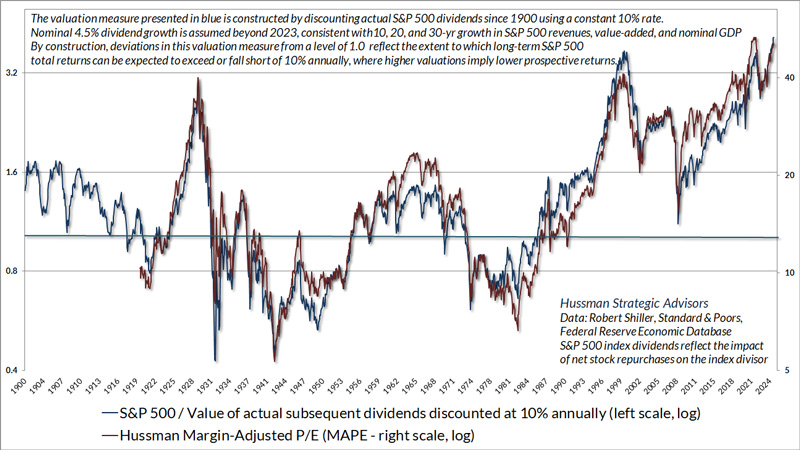

The chart below shows our Margin-Adjusted P/E, which considers cyclical variations in profit margins and their impact on the price/earnings ratio, along with the ratio of the S&P 500 to the present value of actual subsequent S&P 500 dividends at every point in time since 1900, discounted at a constant rate of 10% annually (see chart text for additional details). The ratio therefore estimates the extent to which likely long-term S&P 500 total returns are likely to depart from a 10% average return. The higher the valuation, the larger the expected shortfall from historically run-of-the-mill expected returns of 10%.

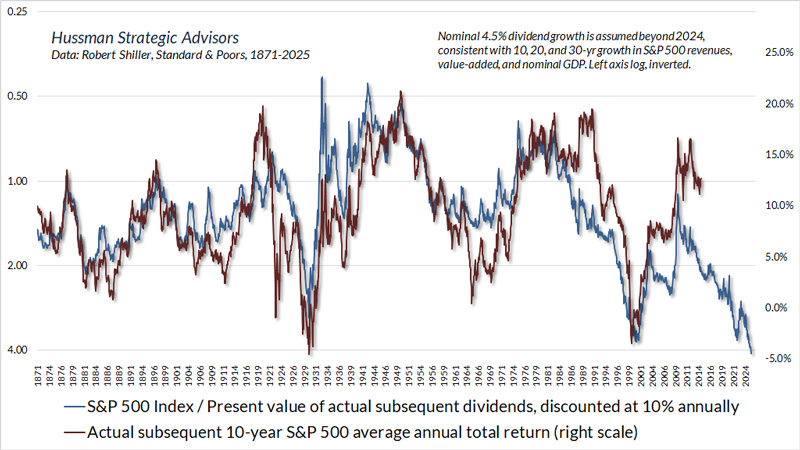

The chart below shows how our S&P 500 dividend discount model above is related to actual subsequent S&P 500 total returns in data since 1871. The relationship clearly isn’t perfect. As with every good valuation measure, the “errors” typically reflect extreme valuations at the endpoint of a given investment horizon. For example, actual 10-year market returns (red) were substantially higher than expected returns (blue) in the 10-year period beginning in 1919. The reason is that the endpoint of that 10-year horizon was the 1929 bubble peak. Likewise, actual 10-year market returns were substantially lower than expected returns in the 10-year period beginning in 1922, because the endpoint of that 10-year period was the 1932 market low.

You’ll see that same feature of “errors” across history. Actual 10-year market returns were substantially lower than expected returns in the 10-year period beginning in 1964, because the endpoint of that 10-year horizon was the 1974 secular valuation low. Actual 10-year market returns were substantially higher than expected returns in the 10-year period beginning in 1990, because the endpoint of that 10-year horizon was the 2000 bubble peak. Put simply, these so-called “errors” contain information. It’s enormously tempting to imagine, at bubble highs, that glorious backward-looking returns, far greater than those previously implied by valuations, demonstrate that historical standards of value are outdated and obsolete. In their 1934 classic, Security Analysis, Benjamin Graham and David Dodd described the mood surrounding the 1929 market peak, observing that investors had abandoned their attention to valuations because “the records of the past were proving an undependable guide to investment.” In truth, there was an enormous warning in the “error” between the returns investors were enjoying and the returns suggested by valuations. Presently, that same kind of “error” offers the same warning as those that misled investors to ignore valuations in 1929 and 2000.

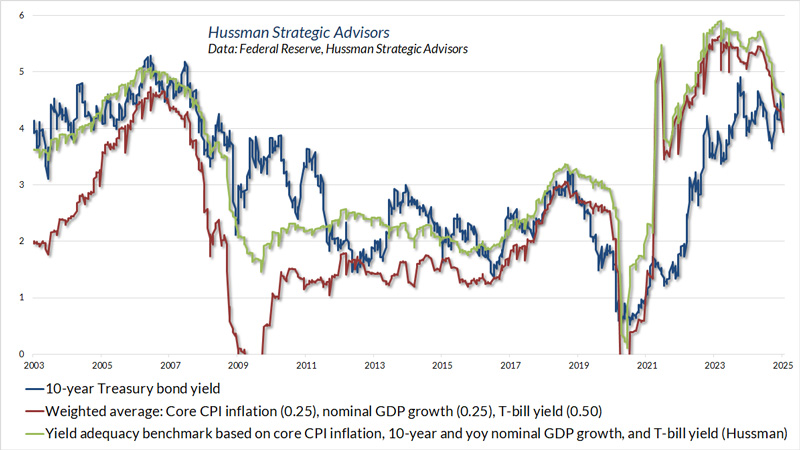

In the bond market, the most notable development in recent weeks is that, after a long period of yields that we’ve viewed as “inadequate,” 10-year Treasury yields have finally pushed to levels that we believe provide reasonable prospects of outperforming Treasury-bill returns. The chart below shows the 10-year Treasury bond yield compared to the simplest of the benchmarks we consider.

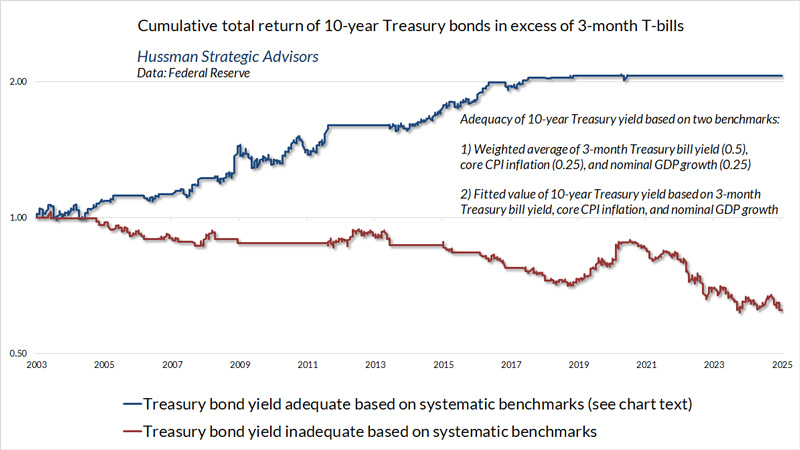

The chart below shows the total return of 10-year Treasury bonds, over-and-above Treasury bill returns, based on whether the prevailing 10-year yield has been adequate or inadequate based on these benchmarks.

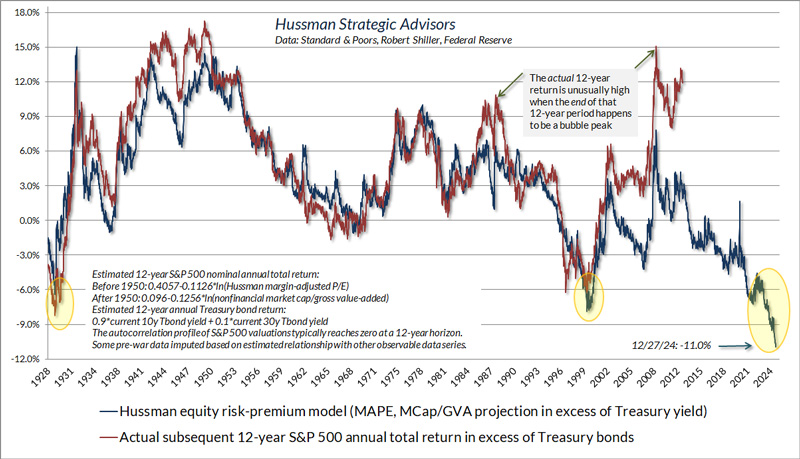

The main update on precious metals shares here is that while we consider valuations to be reasonable, and weaker economic conditions (for example, an ISM Purchasing Managers Index below 50) tend to be better for gold stocks than strong economic conditions, we do consider the recently rising trend of interest rates to be a headwind. More favorable conditions for precious metals shares are likely to emerge when reasonable valuations and relatively weak economic conditions are joined by falling interest rates, even 10-year Treasury yields below, say, their level 6-months earlier. The difference between our estimates of likely 10-year S&P 500 total returns and 10-year Treasury returns – the “equity risk premium” – is currently the widest and most negative in U.S. history. I find it fascinating that so many analysts trot out risk-premium estimates without offering evidence – ideally a century of it – on how those estimates have been related to actual, subsequent outcomes. Investors looking for unsubstantiated verbal bullish reassurance can find this sort of thing easily enough. As for historical evidence – with the emphatic reminder that these estimates say almost nothing about near-term return prospects – the chart below shows the present situation. The reason the estimated gap between expected equity and bond returns is so extreme is because stock market valuations are at record highs while 10-year bond yields are at what we view as historically adequate levels. Again, as always, you’ll see “errors” in this chart, in this case reflecting valuation extremes at the endpoint of certain 12-year horizons. If we assume and rely on market valuations remaining at record extremes 12 years from today, we can also assume that actual equity returns in the coming 12 years, relative to bonds, may be better than our estimate below. Still, even the largest “error” in history would not push the resulting 12-year risk-premium above zero.

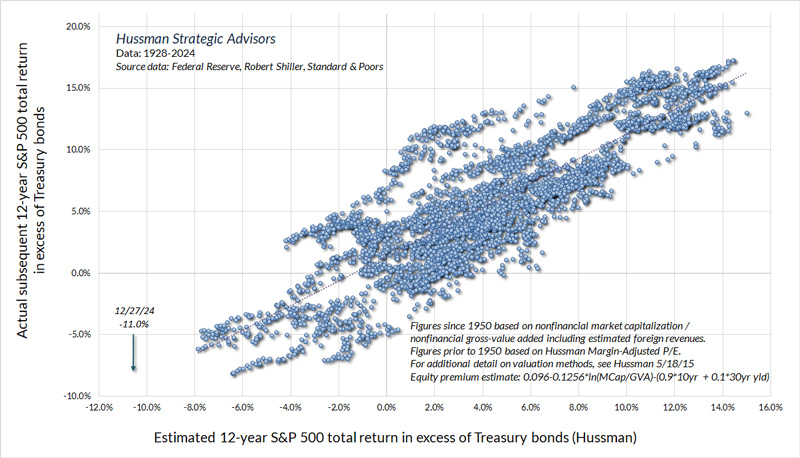

I realize that a shortfall of -11.0% versus bonds seems preposterous and implausible, though I haven’t been a stranger to seemingly preposterous and implausible estimates at the extremes of previous market cycles over the past 40 years. If one wishes to make the implications more tolerable, one can narrow the gap by several percent with heroic but not altogether impossible assumptions about profit margins and growth rates. Unfortunately, my impression is that one has to dispense with history altogether to garner more comfort than that. The chart below shows the same data as a scatterplot.

In short, revailing conditions imply among the most negative prospective returns and deepest potential losses in history. If you look carefully at the bubble, you can already see the collapse within it. Yet turn the TV to the business channel, and at nearly every moment, you’ll find another person with the “unique personal intelligence that tells them that there will be yet more.” Still, as I’ve often noted, if rich valuations were enough to drive the market lower, it would have been impossible to reach extremes like 1929, 2000, and today. The ascent of valuations would have been stopped at lower levels. The only way to get here, at the outer reaches of history, was to advance, undaunted, through every lesser extreme. My impression is that it will end badly, not just because current valuations assume favorable developments, but because they require outcomes that are at odds with history, economics, and financial arithmetic. For more on that point, see the section on “New eras” in Ring Out Wild Bells. It’s unclear how the psychology of investors will unfold in the coming weeks. Our current outlook is bearish, but as I noted earlier, we’re not presently inclined to amplify that should the market advance further. In any event, given that we align our investment positions with measurable, observable conditions as they change over time, no forecasts are required.

|

Send this article to a friend:

|

|

|