Send this article to a friend:

January

15

2024

|

Send this article to a friend: January |

|

| Futures Dip As Doubts Emerge About March Rate Cut,

US equity futures were steady on Monday as investors were displeased by hawkish comments from ECB's Holzmann , who said there may not be any rate cuts this year which pushed European stocks to session lows, while also bracing for more earnings later this week. With cash stock markets closed for Martin Luther King Jr. Day and global liquidity especially thin, S&P 500 and Nasdaq 100 futures were down about 0.1% and unchanged, respectively, as 8:00 a.m. ET, after both underlying benchmarks gained last week as the earnings season kicked off.

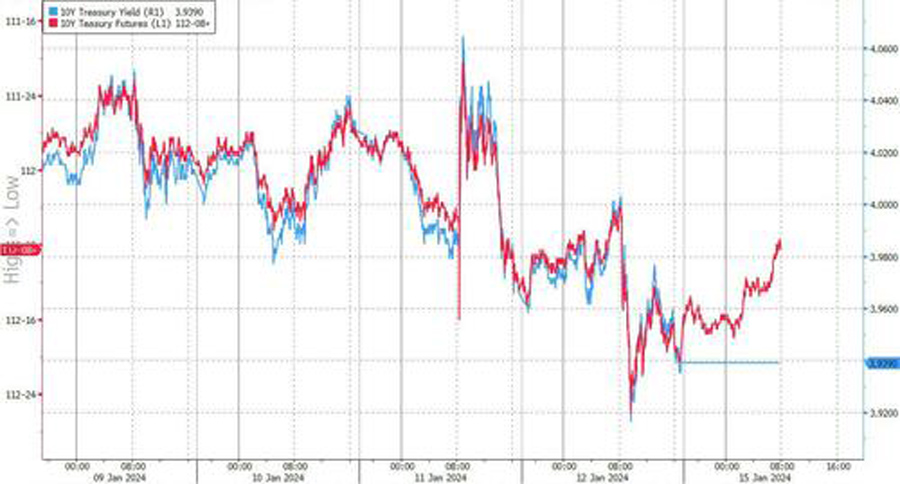

Treasury cash markets are also closed on Monday, although TSY futures suggested yields are higher by about 4bps to 3.98%; the Bloomberg dollar index edged higher following weekend news that a government shutdown had been delayed until March

The market is taking a breather after it rallied in nine of the past 10 weeks, with the S&P trading near its all-time high on optimism that the Federal Reserve could start cutting interest rates as soon as March (although over the weekend Morgan Stanley warned this is unlikely as "it would take either some serious stress in financial markets or notable downside surprises to inflation, jobs, or both to get a rate cut in March"). But data released last week showed US headline inflation re-accelerated in December, boosting warnings that funding costs may stay higher for longer. "Markets could be jumping the gun when it comes to the likelihood of March rate cuts,” said Michael Hewson, chief analyst at CMC Markets in London. European stocks fell as economic data from Germany underscored the ugly backdrop for corporate profits ahead of a raft of speeches by policy makers at the World Economic Forum in Davos this week. The Stoxx Europe 600 index dropped 0.3%, trading at session lows and extending a lackluster start to the year after a 13% rise in 2023. Consumer goods and carmakers led the decline after Germany’s economy dodged a recession, though the latest data showed it contracted for the first time since the pandemic last year. Germany’s 10-year yield rose about five basis points as bonds across the euro region fell as the ECB's Holzmann. “Today’s data could encourage the ECB to speed up monetary easing but we’re now getting at the stage when bad economic news no longer translates into good news for equity markets,” said Benoit Péloille, chief investment officer at Natixis Wealth Management. In the US, market pricing for as many as six quarter-point rate cuts “can be a stretch; bad economic news will start to hurt,” he said. Among individual stock moves in Europe, Dassault Aviation SA slumped after the French aircraft maker reported a decline in 2023 jet orders. Delivery Hero SE and Just Eat Takeaway.com NV dropped after BNP Paribas Exane analysts recommended steering clear of Europe’s food delivery sector. Volvo Car AB extended a decline sparked Friday when it said it’s temporarily halting some production due to shipping delays caused by Red Sea attacks. Earlier in the session, the MSCI Asia Pacific share index climbed for a third session. Stocks advanced in Taiwan after the Democratic Progressive Party won the presidential election and the more China-friendly Kuomintang gained too few seats to control the assembly. Meanwhile, the gong show that is China continued, with the CSI 300 Index swinging between gains and losses amid speculation officials may lower the required reserve ratio after the People’s Bank of China unexpectedly left the rate on its one-year policy loans at 2.5% Monday. That was contrary to expectations among economists that it would trim the so-called medium-term lending facility by 10 basis points. “Rate cuts are likely still on the cards, but China looks to be taking a more measured approach to policy easing,” said Marvin Chen, an analyst at Bloomberg Intelligence in Hong Kong. Well they better be because otherwise Beijing is looking at a mass revolt of a population facing a grim and recessionary economy and imploding capital markets. In FX, the Bloomberg Dollar Spot Index rises 0.2%. The kiwi is the weakest of the G-10 currencies, falling 0.8% versus the greenback. The yen drops 0.6%. In rates, bunds fall as economists still doubt the ECB will cut interest rates as much as market pricing currently suggests. German 10-year yields rise 3bp to 2.21%. In commodities, oil prices decline, with WTI falling 0.8% to trade near $72.10, as the risk that air strikes by the US and allies against the Houthis would ignite a wider conflict and disrupt crude flows from the Middle East was balanced by soft fundamentals. Spot gold adds 0.2%. The US is closed for the MLK day holiday today, and there are no official data releases. Looking at the week ahead, along with more US earnings reports, investors this week will be focused on inflation readings in Germany and the UK, as well as a swath of political leaders and officials including Chinese Premier Li Qiang attending the annual WEF. A speech by Federal Reserve Governor Christopher Waller, after officials last week attempted to temper any expectation of a looming rate cut, will also be closely watched. Top Overnight News

A more detailed look at global markets courtesy of Newsquawk APAC stocks were mostly rangebound after the lack of significant catalysts over the weekend and with global markets set for a quietened session on Monday owing to the extended weekend stateside. ASX 200 lacked direction as strength in energy and telecoms offset the weakness in miners and defensives. Nikkei 225 continued on its upward trend and briefly reclaimed the 36,000 level for the first time since 1990. Hang Seng and Shanghai Comp were choppy after the PBoC refrained from cutting its 1-year MLF rate. Top Asian News

The Stoxx Europe 600 extends earlier losses to fall as much as 0.4%, with autos and banks driving weakness. Among cyclical sectors: banks -0.8%, autos -0.7% and retail -0.7% the laggards; travel +0.7% is a rare bright spot. US futures slightly weaker, with S&P 500 contracts down 0.1%, Nasdaq 100 futures little changed; cash trading closed for a holiday Top European News

Geopolitics: Middle East

Geopolitics: Other

FX

Fixed Income

Commodities

DB's Jim Reid concludes the overnight wrap It’s a US holiday today (Martin Luther King Day), so it will be a very quiet start to the week. My wife was away at a spa weekend so I’m worn out from shouting at the kids non-stop for 2 days so its a shame I’m not in the US for a break. Although it’ll be quiet, we do have the Iowa Caucus during what is a brutally cold spell in the state with -25C forecast for the vote tonight that traditionally kick-starts the election campaign. The key things to watch are whether Donald Trump can get above the psychological 50% share of the Republican vote (the level recent polls suggest he’s hovering around in the State), and/or how close either Ron DeSantis or Nikki Haley can get to him. While there is clearly a long way to go until November, this will give us some early idea of how successful and deep into the primaries Donald Trump’s opposition for the nomination might go. Staying with politics, on Saturday, Lai Ching-te of the incumbent DPP won the presidential election in Taiwan, as expected, with 40.1% of the vote, ahead of KMT’s Hou Yu-ih. Attention is likely to turn to the risks of increased tensions between Taiwan and mainland China, with Bejing’s officials having referred to Lai as a “troublemaker” and “separatist” ahead of the election. So far there hasn't been any escalating rhetoric from the winning party or from China so markets will probably see the immediate tail risk as reduced although this is something that probably bubbles under the surface for a long time ahead. For more information on the context of what is at stake, Marion Laboure and Cassidy Ainsworth-Grace published a presentation pack on the election and surrounding issues last week. See the full report here . The other geopolitics to watch out for are those around the US/UK strikes against Houthi rebels in Yemen towards the end of last week. In terms of the rest of the week ahead, the highlight is likely to be US December retail sales on Wednesday which will have a impact on Q4 GDP forecasts and momentum into Q1. Housing starts and permits (Thursday) and existing home sales (Friday) will also sharpen those forecasts. The latest UoM consumer survey is out Friday, including the latest inflation expectations series which has moved markets in recent months. Our economists point out that in a week of lots of Fed speak, Waller tomorrow (11am EST) might be the most important as his dovish shift in November helped spark the momentum towards the Fed’s dovish pivot. Earnings season will also slowly build in the US too this week. In addition, US lawmakers will vote after today's holiday on yet another stopgap spending bill to avert a partial government shutdown this Saturday. It seems they are pushing this into March. So no doubt we'll be in a similar position again then. In Europe, UK labour market indicators (tomorrow), inflation data (Wednesday) and retail sales (Friday) will be of interest, especially the CPI data. Over in the continent, notable indicators will include industrial production for the Eurozone today and the ZEW survey for Germany tomorrow. Davos also kicks off today so expect lots of headlines and Canada Goose jackets on your business TV screens. Moving on to Asia, the focus in Japan will be on the national CPI release on Thursday and China’s Q4 GDP and December economic activity indicators on Wednesday. Check out the full week ahead calendar at the end as usual with key data, speaker and earnings releases flagged. Asian equity markets are mostly trading higher this morning with the Nikkei (+1.16%) again leading gains, while Chinese stocks are recovering from earlier losses with the CSI (+0.17%) and the Shanghai Composite (+0.36%) moving higher even after the PBOC left its medium-term policy loans rate unchanged (more on this below). Elsewhere, the KOSPI (-0.07%) is swinging between gains and losses with the Hang Seng (-0.15%) seeing minor losses. US stock futures are flat with cash Treasury trading closed due to today's holiday. Coming back to China, the PBOC defied market expectations for a cut as it held the rate on some 995 billion yuan ($139 billion) worth of one-year medium-term lending facility (MLF) loans intact at 2.50%. The MLF was last cut in August 2023, from 2.65%. Recapping last week now. Despite the upside surprise to the CPI on Thursday, investors grew increasing confident that the Fed is likely to cut rates soon, with the CPI details suggesting more moderate PCE inflation, the Fed’s preferred gauge. This momentum continued on Friday after data showed a greater-than-expected decline in the PPI. US December PPI fell -0.1% (vs 0.1%) month-on-month and rose 1.0% in year-on-year terms (vs 1.3% expected). With some measures in the PPI, like healthcare and portfolio management, also captured in the core PCE, a weaker PPI therefore implies a softer core PCE print and greater justification for the Fed to cut rates. Off the back of this, investors raised their expectations of a 25bps Fed cut by March, rising from 78% to 83% on Friday, up from 63% at the start of the week. And 168bps of cuts are now priced it by end-2024, 30bps more than a week earlier. So that’s nearly seven 25bps cuts now expected by the market from the Fed this year. With the soft producer price data reinforcing Fed cut bets, 10yr Treasury yields declined by -2.6bps on Friday, and -10.6bps on the week to 3.94%. The short-end outperformed, as 2yr yields fell -10.2bps to 4.15% (-23.7bps week-on-week), their lowest level since last May. The bond rally was driven by real rates, with the 10yr real yield down -15.7bps and the 2yr -32.2bps on the week. By contrast, 10yr breakevens (+4.1bps Friday and +5.1bps over the week), reached their highest level since November at 2.28%. Over in Europe, 10yr bund yields fell -5.0bps on Friday but rose +2.8bps in weekly terms. Equities fluctuated on Friday but rallied over the week, supported by the rates rally. The S&P 500 gained +1.84% last week (+0.08% Friday), ending the week just 0.3% below its record high at the start of 2022. Soft earnings releases by several US banks on Friday drove the S&P 500 Banks index down -1.27% on Friday, and -3.37% in weekly terms. The tech-heavy NASDAQ outperformed, up +3.09% over the week (+0.02% on Friday) in its largest weekly move up since the start of November. Gains were largely driven by the tech giants, as the Magnificent Seven index of megacap stocks rose +4.25% (-0.16% on Friday). In Europe, the STOXX 600 jumped +0.84% on Friday but traded near flat (+0.08%) on the week. Lastly in commodities, geopolitical risks returned to the fore after the US and UK launched air strikes against Houthi rebels in Yemen. With risks escalating for Red Sea commercial shipping, Danish fuel-tanker company, Torm, announced its intention to pause transits through the Southern Red Sea on Friday. These developments drove Brent Crude prices above $80/bbl in early trading on Friday, before finishing the day at $78.29/bbl (+1.14% on the day). That said, they were down slightly (-0.60%) on the week after an earlier decline on news of Saudi Arabia lowering its selling price. WTI crude similarly rose +0.92% on Friday to $72.68/bbl but was down -1.53% on the week. Rising geopolitical risks in the Middle East also saw gold rally +1.72% on Friday (+0.18% on the week)

|

Send this article to a friend:

|

|

|