Send this article to a friend:

January

08

2024

|

Send this article to a friend: January |

|

What the Fed Accomplished: Distorted the Economy,

Let’s summarize what the Federal Reserve accomplished since embarking on its massive interventions to control volatility, risk, bond yields, interest rates, the mortgage market, bank subsidies and liquidity, all of which can be summed up as the cost of credit-capital, that is, capital that is borrowed into existence based on some form of collateral or income stream. By artificially suppressing the cost of capital to less than inflation, the Fed succeeded in:

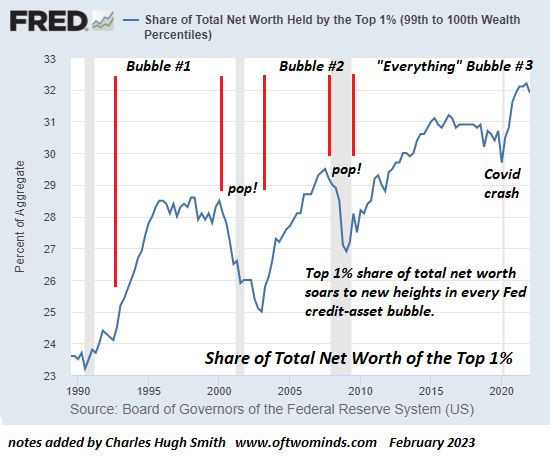

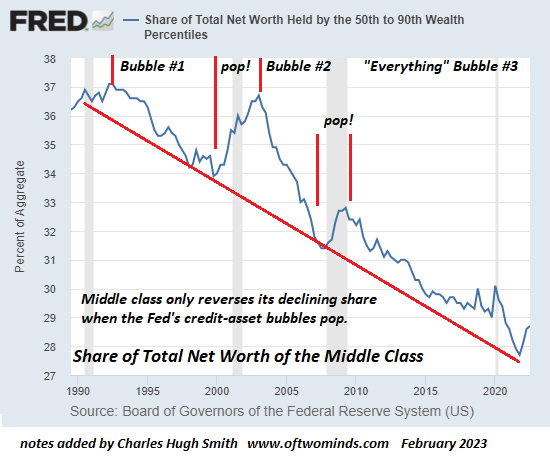

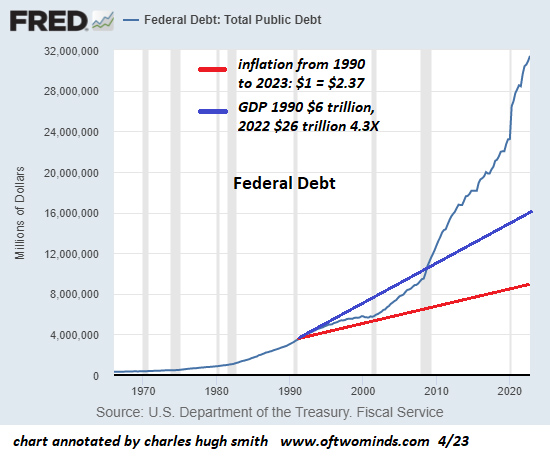

Let’s consider how the Fed fatally distorted the economy by suppressing the cost of capital to less than inflation. Recall that the Fed crammed ZIRP–zero interest rate policy–down the throat of the economy from 2009 to 2020, while official inflation ate up 22% of the purchasing power of the dollar. Inflation was never 0%, so the cost of capital for corporations and financiers was actually negative, i.e. less than inflation. Reducing the cost of capital had multiple distorting effects. A useful analogy is the critical role of “keystone species” in maintaining healthy, diverse ecosystems. Risk and competition are the vital forces enabling a diverse ecosystem. Once the keystone predators have been eliminated (starfish, wolves, et al), the species freed from risk and competition overwhelm the ecosystem and crowd out healthy diversity. These species end up destroying the ecosystem via overgrazing, destruction of forests, etc. The same dynamic, enforced by the Fed, has gutted the US economy. Corporations and financiers with virtually unlimited access to near-zero cost capital were freed to buy up hundreds of smaller competitors, buy back trillions of dollars of their own shares to enrich the already rich managers and large shareholders and leverage their assets and cash flow into Empires of Debt which could be sold or taken public (WeWork, et al) reaping enormous profits–profits unavailable to wage earners and those who did not have the opportunity to acquire assets before ZIRP inflated the Everything Bubble. It’s been estimated that the majority of the S&P 500 / stock market’s rise from 667 in 2009 to current levels around 4,700 was solely the result of corporate buybacks that reduced the number of shares. This artificially increased the revenues and earnings per share. (Buybacks were once illegal, for good reason.) All these trillions in near-zero cost capital flowed into manipulation, speculation and the reduction of competition, not into boosting productivity, efficiency or innovation. The net result of the Fed’s ZIRP is an economy stripped of diversity, an economy dominated by bloated monopolies, cartels and platforms generating low-quality, addictive goods and services which reduce productivity on multiple fronts. Lowering the cost of capital to near-zero also changed the incentives of corporate and banking leaders. The enormous profits flowed not from developing higher quality goods and services or improving customer service; they flowed from manipulating markets with near-zero cost capital, borrowing fortunes against corporate commercial real estate and distributing the gains to shareholders and managers. Near-zero cost capital rewarded speculators and CEOs who leveraged financier plays, not those investing for the long-term in America. The Fed’s distortions are fatal because they stripped the economy of incentives that are positive for the nation, not just for corporations and the already-wealthy. Lowering the cost of capital to zero also distorted the balance between labor and capital in favor of capital, as the already-wealthy, i.e. those who already owned collateral and cash flows, could leverage up their assets and income to borrow vast sums at near-zero interest to scoop up income-producing assets. Mere wage earners could not compete and so wealth and income flowed to the top 01%, top 1% and top 10%:

|

Send this article to a friend:

|

|

|

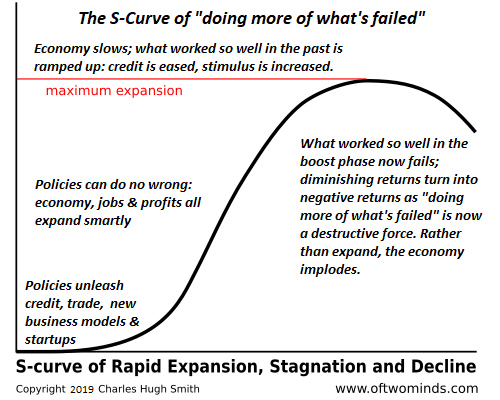

The mainstream holds the Fed is busy planning a return to the glory days of zero interest rates, but ZIRP is on the downside of the S-Curve; it’s done, gone, history.

The mainstream holds the Fed is busy planning a return to the glory days of zero interest rates, but ZIRP is on the downside of the S-Curve; it’s done, gone, history.